One platform, zero friction

Consolidating separate online and offline systems into a unified platform. Part of the team that bridged siloed data streams, automated manual financial reconciliation, and eliminated cross-channel operational friction.

background.

Our payment ecosystem supported thousands of enterprise partners across two primary channels: offline POS and online e-commerce. As the network scaled, managing these dual revenue streams on entirely disconnected legacy platforms became an unsustainable operational bottleneck.

Problem.

Because the online and offline platforms operated in silos, the friction was two-sided:

- Externally

Enterprise chains wrestled with fragmented account logins across systems, and their finance teams spent days manually cross-referencing omnichannel data to close their monthly books.

- Internally

Maintaining two codebases doubled the engineering overhead. More critically, our operations team was trapped doing manual monthly billing and processing cross-channel refunds by hand.

Goal.

Architect a unified omnichannel merchant platform that consolidated online and offline data streams, simplified enterprise account hierarchies, and automated cross-channel financial reporting — all with zero disruption to daily partner revenue.

Contribution.

- Omnichannel product strategy

- Enterprise account hierarchy design

- Self-serve financial ops & refund design

- Phased partner migration planning

the decisions.

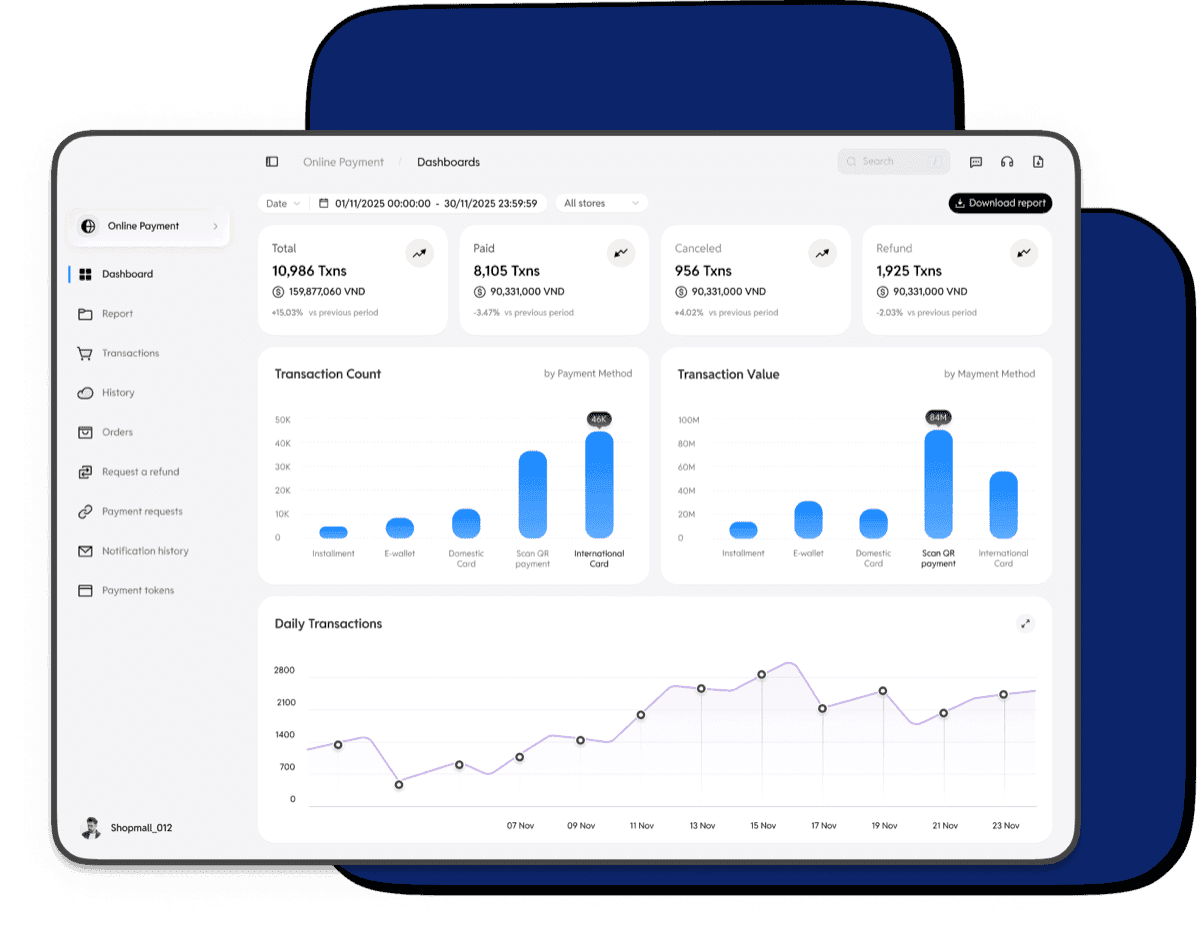

The project began as an effort to unify two legacy platforms, but discovery revealed a critical breakdown in our enterprise partners' daily operations. Retail chains were manually stitching together offline store transactions and online e-commerce revenue to close their books — a grueling process highly prone to human error and constant data conflicts. It became clear that we couldn't just build a consolidated dashboard; we had to architect a completely new financial engine. We reframed the product vision around data integrity: automating the cross-channel reconciliation process to solve enterprise operational friction at its root.

The 'Feature Parity' Trap — Over the years, both legacy platforms had grown a long tail of highly customized, edge-case features built for specific enterprise clients. As we build the new unified platform, how do we handle this legacy?

Pick the move you would make — you can change your answer.

API-First vs. Dashboard — We know enterprise finance teams need this omnichannel data to close their books. However, engineering bandwidth is limited. Where do we focus our initial development effort to deliver the most business value?

Pick the move you would make — you can change your answer.

The Portal is live and most partners have adopted it — but a segment of merchants, after months of recommendations, still won't switch. They're comfortable with what they know. How far do we push?

Pick the move you would make — you can change your answer.

Details and figures have been generalized.

outcome.

We replaced siloed online and offline platforms with a centralized financial engine, eliminating the manual cross-channel reconciliation cycle for our enterprise partners. The entire partner base migrated with minimal churn. The grueling manual month-end ops cycle was replaced by an automated, real-time settlement view and a lightweight review queue.

Takeaways

Impact.

Manual reconciliation eliminated: the month-end close cycle went from days of manual cross-referencing to an automated settlement view. The entire partner base migrated successfully with minimal churn. The unified data architecture significantly reduced the internal support surface and gave retail headquarters real-time, conflict-free settlement visibility for the first time.

What I learned.

What looked like a standard system migration was actually a business process transformation. Shadowing enterprise finance teams revealed the real pain was the structural data conflict between local offline operations and corporate e-commerce. Architecting for data integrity first made the front-end UI migration feel almost incidental.

Next steps

- 1

Extend the centralized refund engine to cover complex cross-bank settlement disputes, which still require manual ops intervention.

- 2

Evaluate rolling out the unified financial engine to the insurance partner segment, which currently runs on a third legacy system.